What is the Image Guided Radiotherapy Market Overview – definition, scope, and significance?

Image Guided Radiotherapy (IGRT) refers to the integration of advanced imaging technologies with radiation therapy devices to precisely locate tumors and adapt treatment delivery in real time. The market encompasses hardware such as linear accelerators equipped with imaging modules, software platforms for treatment planning, and related services. Its scope spans hospitals, oncology centers, and dedicated radiotherapy facilities worldwide. The significance lies in enhanced treatment accuracy, reduced toxicity, and improved patient outcomes, driving higher adoption across cancer care pathways.

What are the Image Guided Radiotherapy Market Drivers, restraints, challenges, and opportunities?

Key drivers include rising cancer incidence, increasing demand for minimally invasive therapies, and rapid technological advancements in MRI, CT, and PET imaging. Growth is further propelled by expanding reimbursement frameworks and heightened awareness of precision medicine. Restraints stem from high capital costs, limited skilled personnel, and stringent regulatory approvals. Challenges involve integrating multi‑modal imaging data and ensuring interoperability across platforms. Opportunities arise from emerging AI‑driven segmentation tools, portable imaging solutions, and emerging markets seeking modern oncology infrastructure.

What are the current Image Guided Radiotherapy Market growth trends?

Current trends feature a shift toward hybrid imaging‑radiotherapy systems that combine MRI or PET with linear accelerators, enabling real‑time tumor tracking. There is also a notable rise in adaptive radiotherapy protocols, where treatment plans are modified based on daily imaging feedback. Vendors are increasingly offering bundled product‑service contracts, and cloud‑based treatment planning platforms are gaining traction for collaborative care. Additionally, the market is witnessing growth in outpatient radiotherapy centers that leverage IGRT for shorter treatment cycles.

How has COVID‑19 impacted the Image Guided Radiotherapy Market and what is the recovery trajectory?

The pandemic caused temporary delays in elective cancer procedures, leading to a short‑term dip in equipment installations. However, the need for remote treatment monitoring accelerated adoption of tele‑oncology and AI‑enabled imaging analysis. Post‑2022, demand rebounded strongly as hospitals prioritized oncology services, resulting in a robust pipeline of new contracts. The recovery trajectory is upward, supported by postponed projects and renewed investment in resilient healthcare infrastructure.

What does the Image Guided Radiotherapy Market competitive landscape look like?

The competitive landscape is characterized by a few large OEMs and several specialized innovators. Major players such as Accuray Incorporated, Elekta AB, GE Healthcare, Siemens AG, and Varian Medical Systems dominate hardware sales, while companies like Vision RT Ltd. focus on motion‑management software. Recent years have seen strategic mergers and joint ventures to broaden product portfolios, leading to moderate market consolidation and intensified competition on technology differentiation and service models.

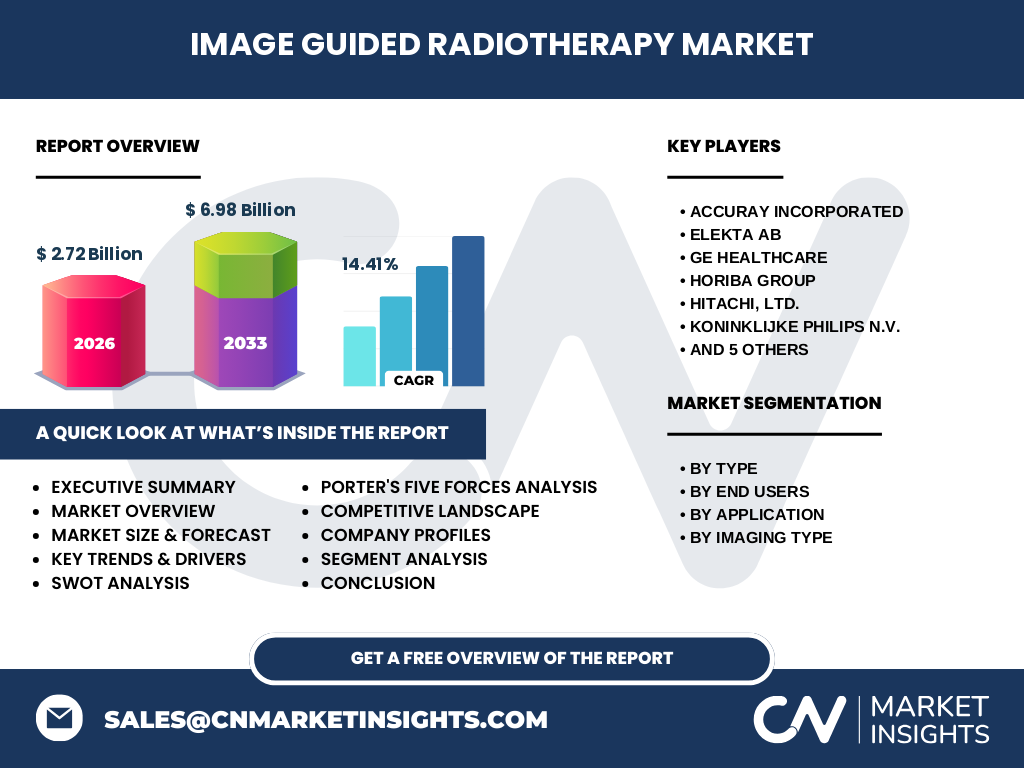

Can you provide an executive summary of the Image Guided Radiotherapy Market?

The Image Guided Radiotherapy market is valued at $2.72 billion in 2026 and is projected to reach $6.98 billion by 2033, reflecting a CAGR of 14.41 %. Growth is driven by rising cancer prevalence, technological integration of MRI/CT/PET with linear accelerators, and expanding adoption in hospitals and specialized oncology centers. While high upfront costs and regulatory hurdles pose challenges, AI‑enabled solutions and emerging regional demand present significant upside. The market remains highly competitive, with leading OEMs pursuing innovation and strategic partnerships.

What are the forecasted market outlook for Image Guided Radiotherapy from 2025 to 2032?

Based on the provided CAGR of 14.41 %, the market is expected to maintain strong expansion through 2032, surpassing the $6.98 billion mark by 2033. Annual growth will be fueled by continued rollout of adaptive IGRT systems, increasing procurement by oncology centers, and broader reimbursement coverage. The forecast anticipates expanding product portfolios, heightened service revenue, and deeper penetration in emerging economies as infrastructure investments rise.

How is the Image Guided Radiotherapy Market sized and shared by segmentation?

Segmentation analysis reveals four primary dimensions. By type, the market is split between products (hardware such as linacs and imaging modules) and services (maintenance, software licensing, and training). End‑user segmentation shows hospitals, oncology centers, and radiotherapy centers as key consumers, each requiring tailored solutions. Application‑wise, demand spans breast, lung, gastrointestinal, prostate, gynecological, and head‑and‑neck cancers, reflecting IGRT’s versatility across tumor sites. Finally, imaging type segmentation includes MRI, PET, and CT, with each modality underpinning specific clinical workflows.

What is the global Image Guided Radiotherapy market size and share by region?

The global market, valued at $2.72 billion in 2026, is distributed across North America, Europe, Asia‑Pacific, and the Rest of World. While precise regional revenue figures are not disclosed, North America and Europe currently hold the largest shares due to mature healthcare systems and early technology adoption. Asia‑Pacific shows the fastest growth rate, driven by expanding cancer care networks and government initiatives supporting advanced radiotherapy.

What does the regional analysis of the Image Guided Radiotherapy market reveal?

In North America, strong reimbursement policies and high hospital density drive robust IGRT installations. Europe benefits from cooperative research programs and standardized clinical guidelines that accelerate market penetration. Asia‑Pacific’s growth is propelled by rising cancer incidences, increasing private hospital investments, and supportive regulatory reforms. The Rest of World, including Latin America and the Middle East, demonstrates incremental adoption as local providers upgrade legacy radiotherapy units to image‑guided platforms.

Which companies lead the Image Guided Radiotherapy market and what are their strategies?

Key players include Accuray Incorporated, Elekta AB, GE Healthcare, HORIBA Group, Hitachi Ltd., Koninklijke Philips N.V., Siemens AG, TOSHIBA CORPORATION, Varian Medical Systems, Inc., ViewRay, and Vision RT Ltd. Strategies focus on expanding product lines with integrated MRI‑linac systems, investing in AI‑driven treatment planning, pursuing strategic alliances for software development, and offering comprehensive service contracts. Many leaders are also accelerating geographic expansion through local manufacturing and distribution partnerships.

How does Porter’s Five Forces analysis apply to the Image Guided Radiotherapy market?

Threat of new entrants is moderate due to high capital intensity and regulatory barriers. Bargaining power of suppliers is relatively low as a few large OEMs dominate component supply, but specialized imaging sensors hold some influence. Bargaining power of buyers is moderate; large hospital networks negotiate volume discounts, while smaller centers have limited leverage. Threat of substitutes is low because alternative cancer therapies cannot replicate the precision of IGRT. Competitive rivalry is high, driven by rapid innovation cycles and the race for integrated imaging‑radiotherapy solutions.

What are the SWOT insights for the Image Guided Radiotherapy market?

Strengths: Proven clinical benefit, strong reimbursement in key markets, and a broad product ecosystem. Weaknesses: High acquisition cost and complex implementation requirements. Opportunities: AI‑enhanced imaging, expansion in emerging economies, and growth of outpatient radiotherapy services. Threats: Regulatory delays, potential market saturation in mature regions, and competition from alternative therapeutic modalities.

What does the value chain of the Image Guided Radiotherapy market look like?

The value chain begins with research and development (R&D) of imaging and radiation technologies, followed by component manufacturing (detectors, gantries, software). Integration and system assembly are performed by OEMs, who then distribute through global sales networks. Post‑sale, the chain includes installation, training, maintenance, and software updates. End‑users—hospitals and oncology centers—deliver the final clinical service, generating data that feeds back into R&D for continual improvement.

What key investment insights can be drawn for the Image Guided Radiotherapy market?

Investors should focus on companies that combine hardware with recurring service revenue, as this hybrid model enhances cash flow stability. Target firms with strong AI and adaptive radiotherapy pipelines, as these technologies differentiate offerings and command premium pricing. Geographic diversification into Asia‑Pacific presents higher growth potential, while maintaining exposure to established North American and European players mitigates risk. Partnerships with imaging specialists also signal long‑term strategic value.

What conclusions can be drawn from the Image Guided Radiotherapy market analysis?

The IGRT market is on a decisive upward trajectory, underpinned by clinical demand for precision, technological convergence, and supportive reimbursement environments. Despite cost and regulatory challenges, the sector’s growth is reinforced by AI‑driven innovations and expanding global cancer care capacity. Stakeholders who invest in integrated solutions, service contracts, and emerging regions are positioned to capture the majority of the projected $6.98 billion market by 2033.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, clinicians, and regulatory experts, with secondary data from peer‑reviewed journals, market databases, and company filings. Quantitative data were validated through cross‑checking against multiple sources, while qualitative insights were coded to identify recurring themes. Forecasting leveraged the specified CAGR of 14.41 % and incorporated scenario analysis to account for macro‑economic and policy variables.

What is the scope of this research?

The scope encompasses global market size, segmentation by type, end‑user, application, and imaging modality, and regional analysis for North America, Europe, Asia‑Pacific, and the Rest of World. It covers competitive dynamics, value‑chain assessment, and strategic recommendations, but does not extend to detailed pricing structures or proprietary clinical trial outcomes. The analysis focuses on the period up to 2033, reflecting the provided forecast horizon.

Which key companies and recent developments define the Image Guided Radiotherapy market?

Leading firms such as Accuray, Elekta, GE Healthcare, Siemens, and Varian have announced new MRI‑linac platforms, AI‑based planning software, and expanded service networks in 2023‑2024. ViewRay introduced a compact cobalt‑based IGRT system targeting low‑resource settings, while Vision RT released an advanced motion‑management camera suite integrated with major linear accelerators. Strategic collaborations between imaging specialists like Philips and radiotherapy OEMs have been highlighted, underscoring a trend toward end‑to‑end solutions.